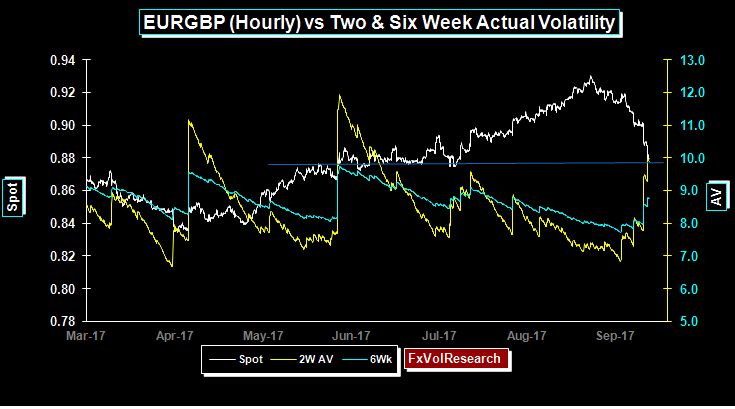

As we forecast here last week EURGBP has corrected lower but the move has been greater than anticipated. Support at 90 has quickly given way to the next support at 88. This looks less like a correction and more like a trend reversal. As pointed out here in the last few weeks the background to this move was seen first in the change in the Labour Party’s approval of an interim agreement following the expiry of the two-year Brexit deadline.

The May government may be forced to re-affirm that some sort of interim agreement basically re-affirming the status quo will be required to bridge a gap following the formal end of the two-year Brexit process. This has predictably caused greater dissent within the Tory party with Boris Johnson’s piece in the Telegraph this weekend is a prime example. Johnson’s op-ed could a view as a prelude to resignation and potentially a challenge to May’s leadership. However, if both of the main political parties are in favor of an interim agreement following the two-year Brexit deadline, then the whole issue of the UK’s relationship with the EU27 will move into the background & the focus will return to UK’s economic fundamentals. Remember, the UK has, so far, only talked about leaving the EU, it still has not happened. So in this period GBP has been cheap, largely because the markets have tended to swallow the governments rhetoric about a hard Brexit.

If Brexit does fade into the background, then the Bank of England will be in a more favorable condition to formulate monetary policy based more on fundamentals. Longer-term indicators using the Vortex indicator have now gone short EUR after being long from levels around 85 back in May of this year. This is not a correction, it’s a reversal. The FX markets have remained somewhat complacent about the potential volatility of both GBP volatility vs the Dollar and the EUR. Further sources of volatility apart from Brexit are the durability of the May government and real possibility of another election.

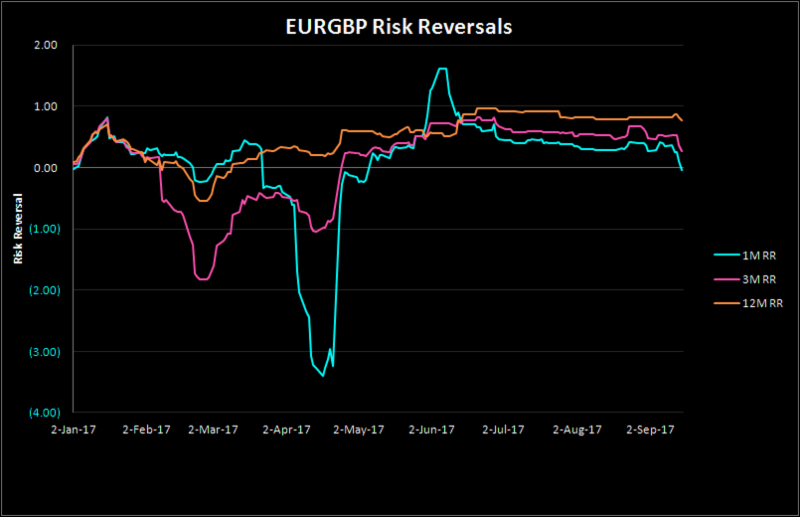

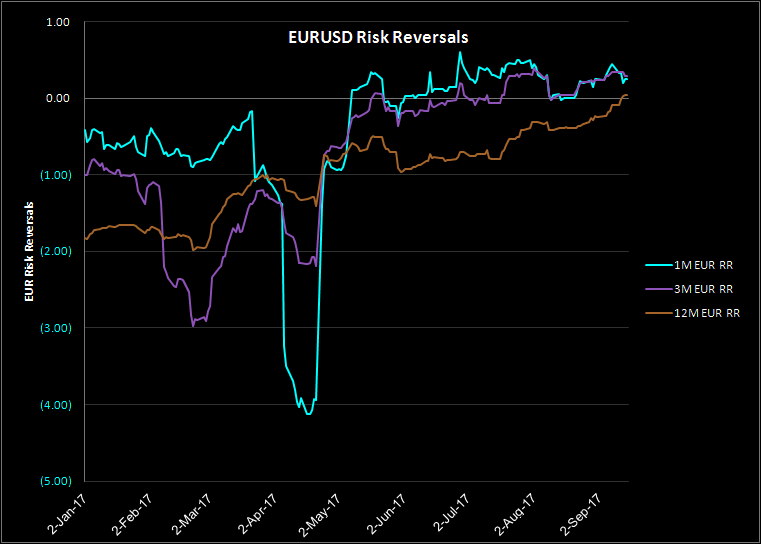

EUR/GBP risk reversals have moved better bid for GBP calls with the one month now showing a small premium for GBP calls, EUR puts. However, the one year remained far more stable with the premium for EUR calls only declining marginally. A good sign that the EUR has peaked will be confirmed once the back end of the RR curve follows the front end lower.

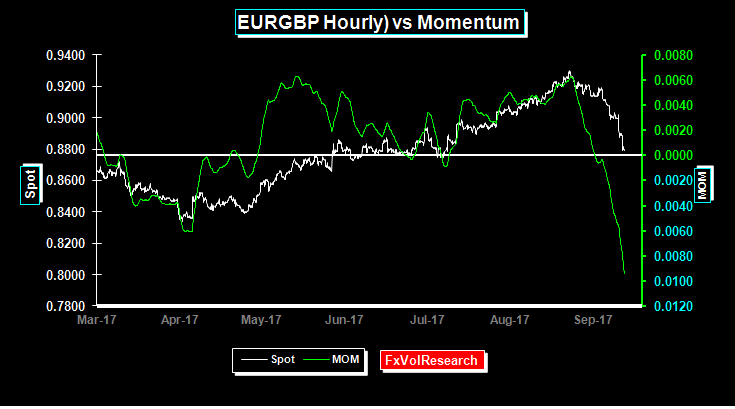

Momentum has predictably collapsed and in the near term at least, looks overdone. Some sort of short-term consolidation is likely following last weeks dramatic sell-off. A close under 88 this week would be another good indication that the EUR rally is over for the near term.

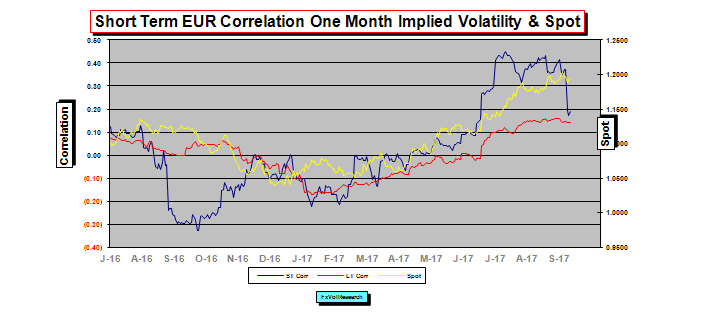

The Short-term correlation of IV and spot is again showing signs of EUR spot price exhaustion. The EUR trend is in need of a larger correction. A good short term correction in the EUR will increase the odds of the EUR rally re-asserting itself.

One year EUR risk reversals are now at a premium for EUR calls, while the one and three months moved slightly lower.

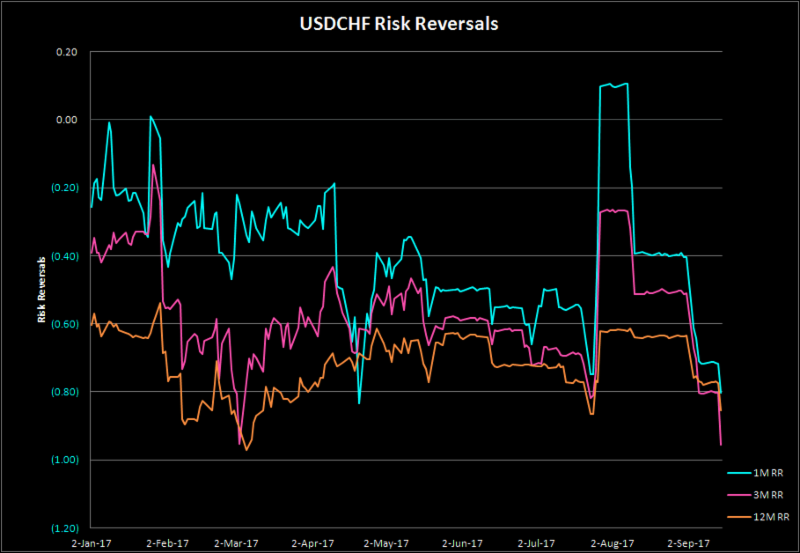

The CHF has been choppy and volatile above the key 94 level which has held on two attempts to break lower. The CHF risk reversal curve moved better bid for CHF calls this week despite the choppy price action. Clearly, the market fears a sustained break under 94 would set off a more sustained & impulsive move lower.

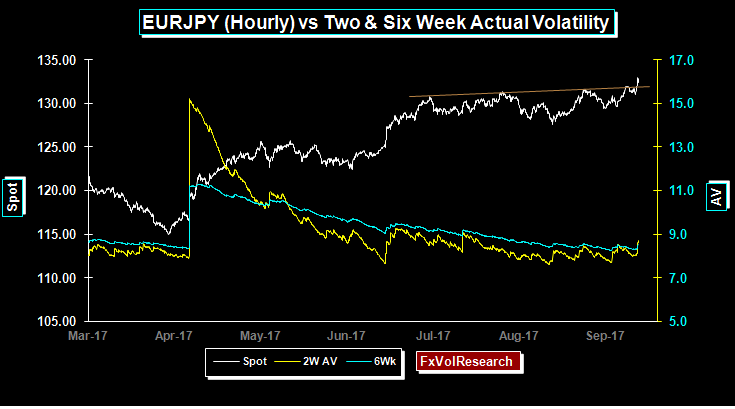

EUR/JPY actual vol has been declining in line with the spot consolidation. That may now be about to change with short-term 2 weeks actual vol trending over the six weeks for the first time in months. Similarly, the spot looks like it may finally be starting to trend higher.

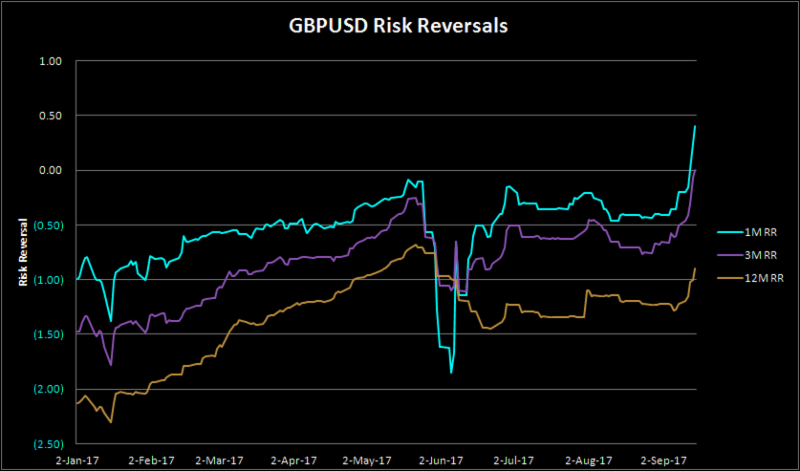

Unsurprisingly, GBP risk reversals all moved better bid for GBP calls, with the front end showing the largest move. Historically GBP risk reversals do not tend to spend a great length of time in positive territory. However with another gap higher in GBP the premiums for GBP calls in the near term will likely trend higher still.

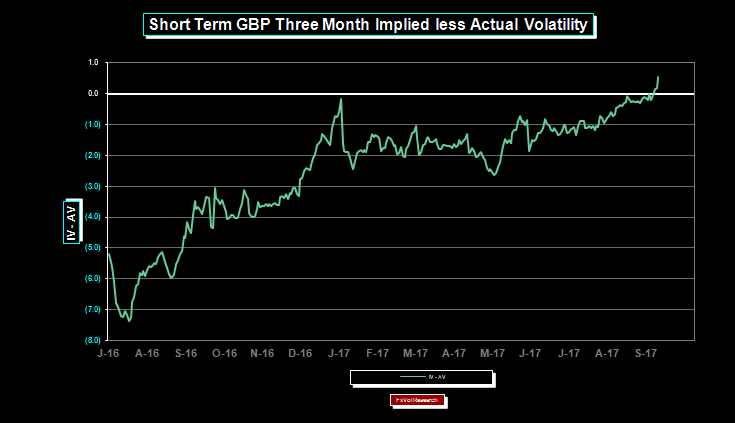

GBP vol has been undervalued for some time with the spreads between implied and actual negative. That changed this week as the three month IV-AV spread has now moved into positive territory.

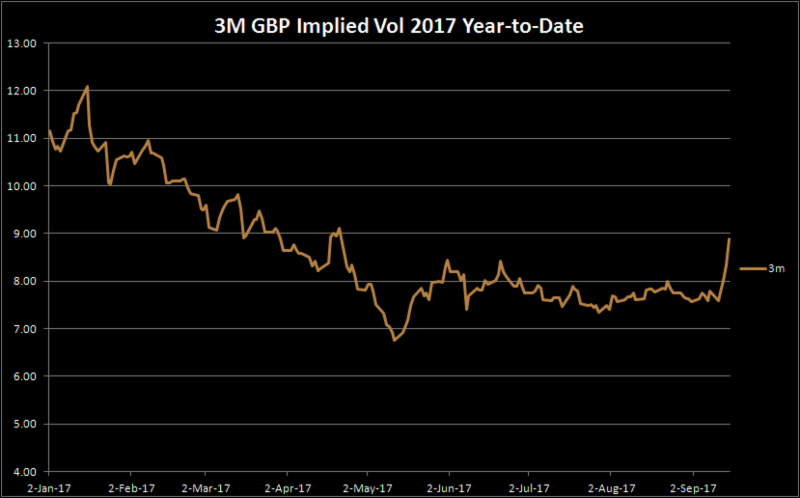

GBP vols bottomed in 2017 just under 7% mid year following a steady decline from 12% at the start of the year. Last weeks move only puts 3M GBP vols in the middle of the year-to-date range.

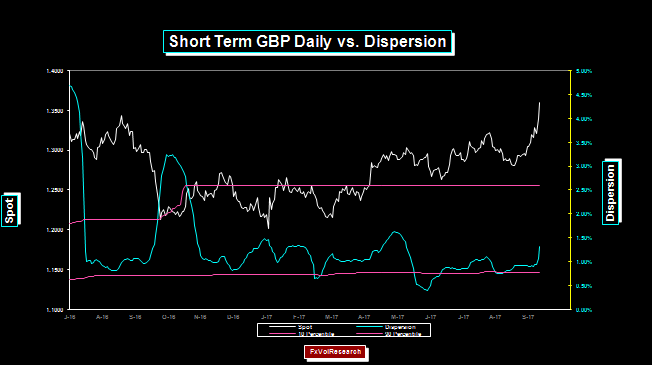

Despite last weeks sharp move in % terms, Dispersion is still low. There is a considerable amount of clear sky above.

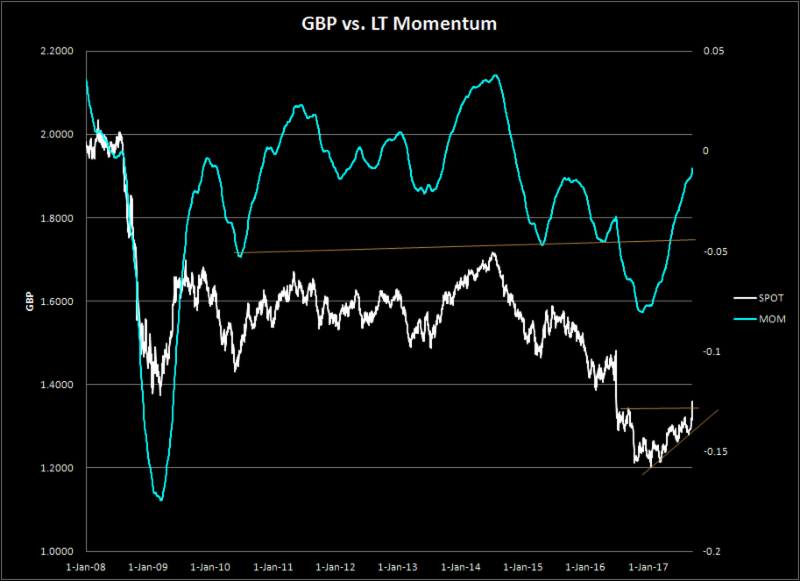

Long-term GBP momentum indicators are almost into positive territory. 1.4000 is the next topside resistance.

Source: James Rider – http://bit.ly/2jC6KaA