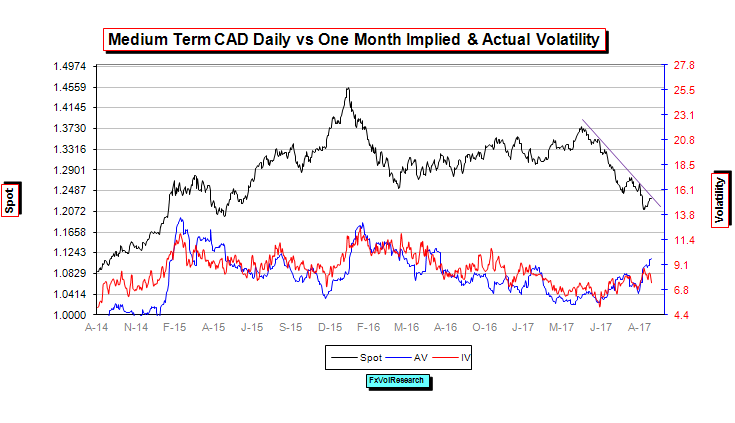

One month CAD vol has come off too far too fast. Same story with the one and two week periods. Gamma options are still worth owning given the spreads with the short term actuals. The one month at levels under 7.4 should prove a good buy particularly as a hedge if you are short the body of the curve.

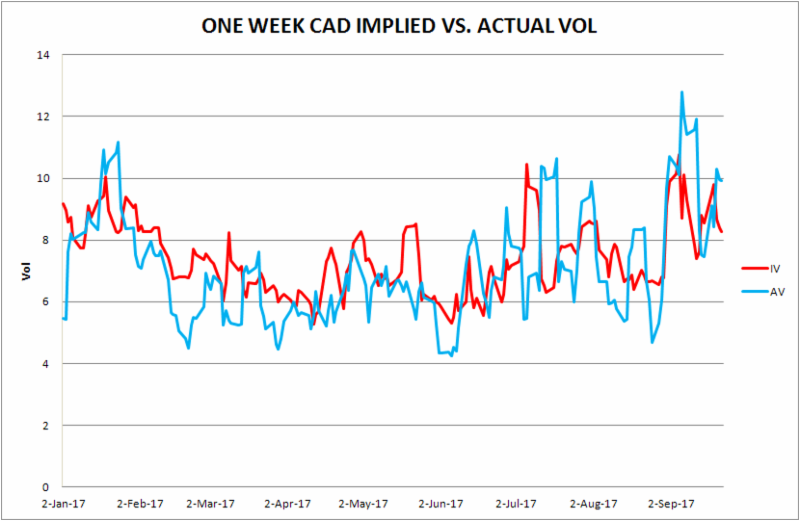

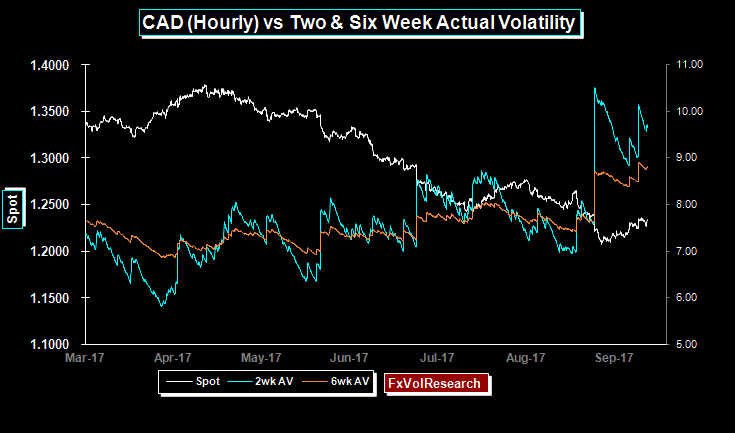

Above is the two and six-week CAD actuals. Gamma style options seem to be underpriced in relation to the recent historical actuals. With the two weeks still well over the 6wk, the options market has got out a bit too far ahead of the curve.

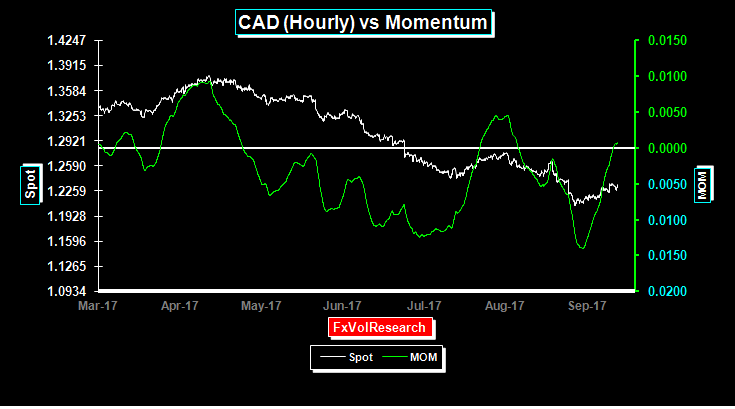

CAD momentum closes barely in positive territory for the US$. The CAD is holding the short term trend line.

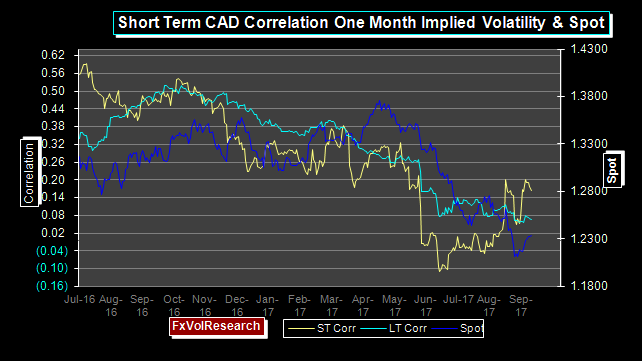

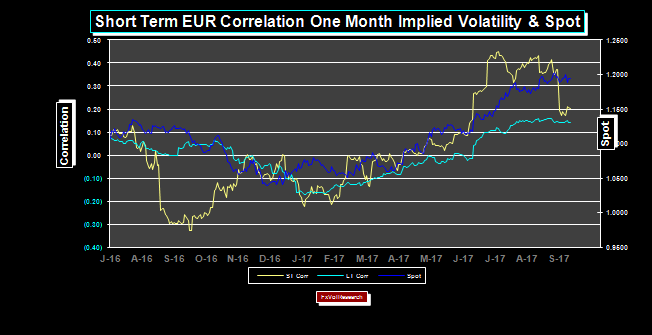

Short-term correlation of spot and implied vol continues to suggest that further CAD strength is limited.

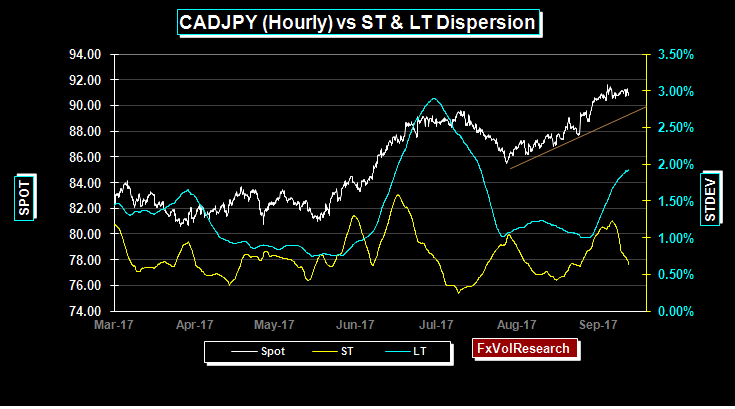

CADJPY takes out the previous cyclical high and holds its trend line. However 6wk dispersion is showing early signs of rolling over and potentially signaling the end of the upside momentum.

Similarly, CADJPY risk reversals moved lower with more demand for Yen calls vs CAD rising at the close of the week.

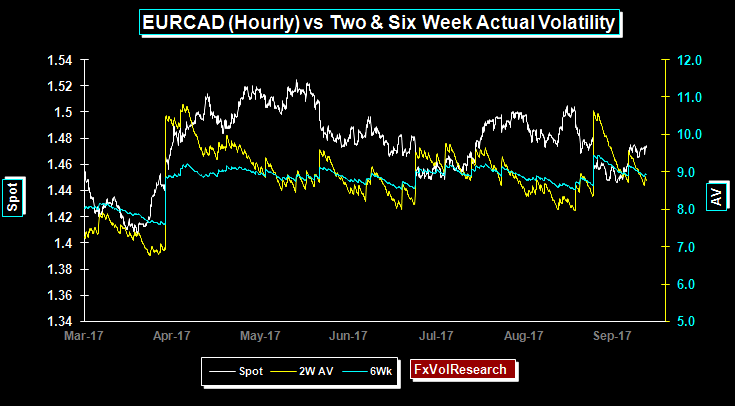

EURCAD actuals are trending lower and more broadly the spread between CADEUR vs EURUSD vols has narrowed. CAD-cross vols generally declined on the week relative to the Dollar based currency pairs.

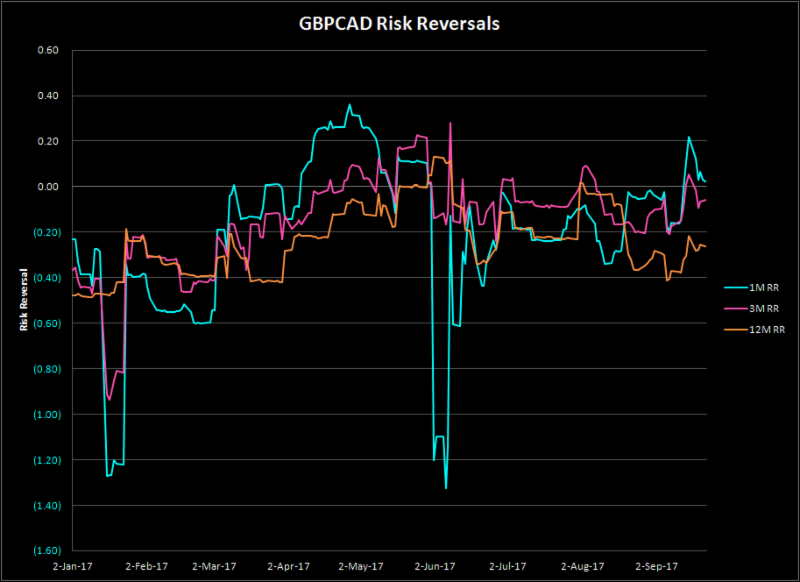

Similar story with GBPCAD with the GBPCAD risk moving lower on the week and GBP calls losing some of their premia.

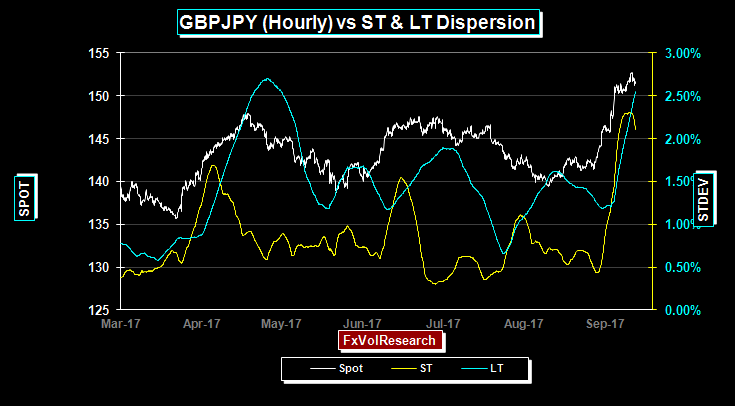

LT GBPJPY dispersion still rising, thus, no clear sign of the GBP rally vs the Yen turning just yet.

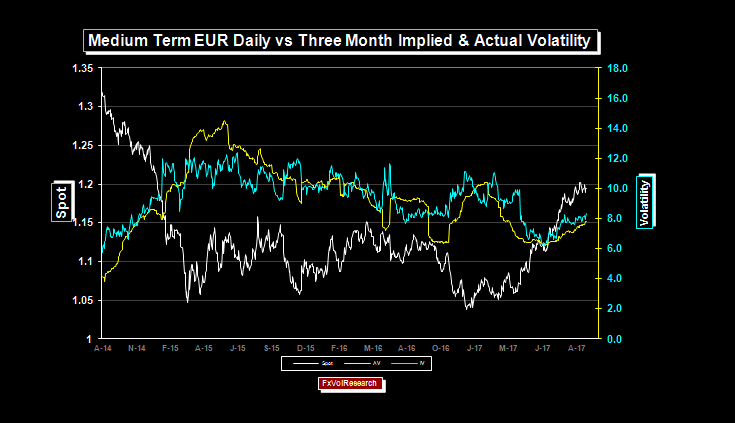

Short-term correlation of EUR IV and spot continue to suggest a correction in the EUR is increasingly likely.

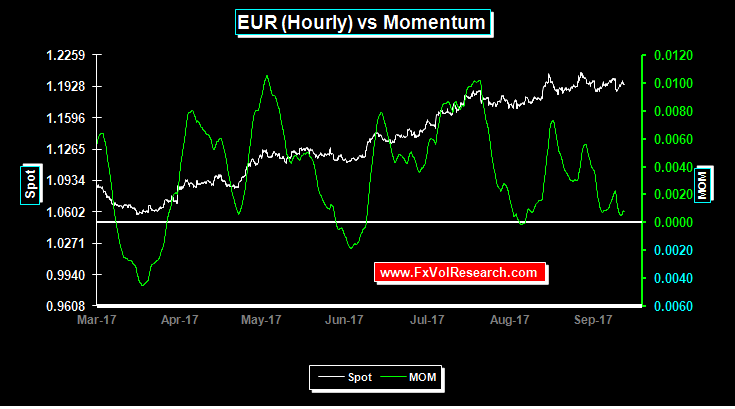

Weak signs of EUR momentum divergence also increase the odds of an EUR correction. As we have said here previously the EUR can correct to 1.1700 and still be in an LT uptrend.

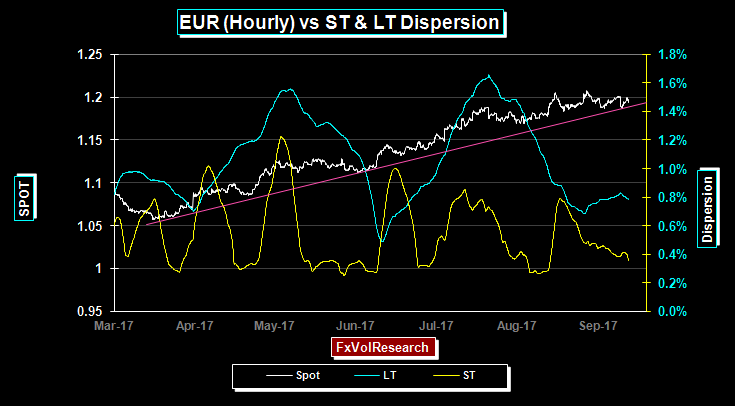

EUR holds it LT trend line.

EUR implied vols still grinding higher, but still not expensive using our own internal indicators.

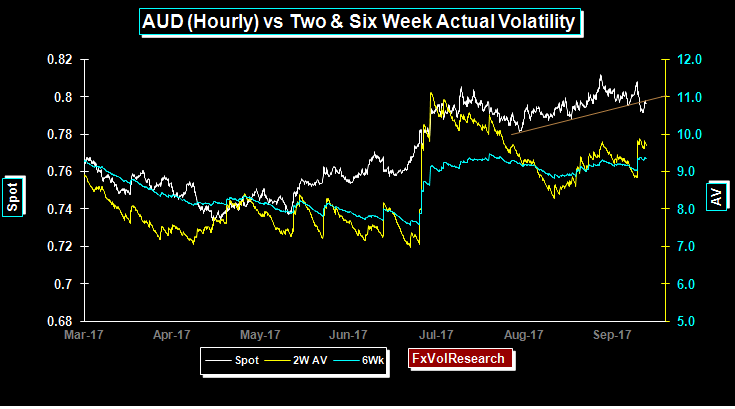

AUD actuals trending high while the spot fails to take out the bottom end of the trend line. As mentioned here previously, unless we are in a global background of accelerating growth and accelerating commodity prices it is hard to see how the AUD can sustain levels above 80cents.

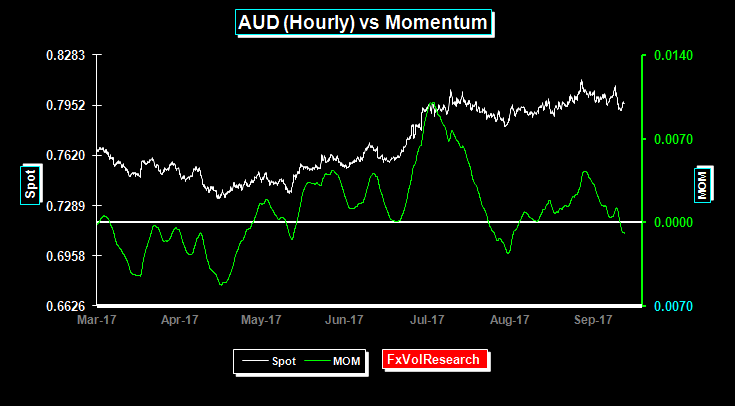

AUD short-term momentum turns modestly negative. Both iron ore and copper prices showed some early signs of rolling over.

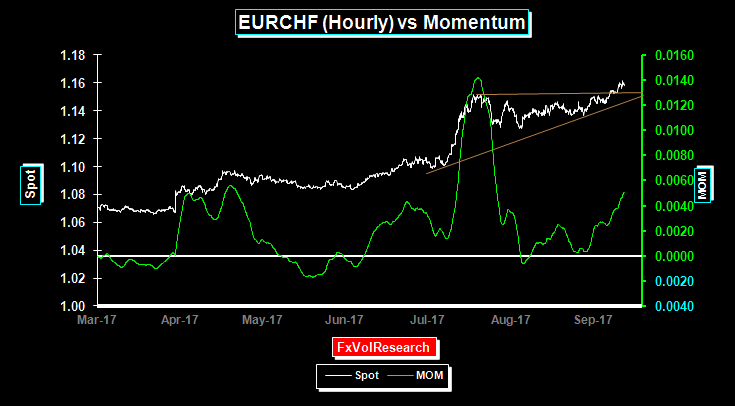

EURCHF breaks out of its triangle formation. Has the EUR replaced the CHF as the go-to currency during periods of risk aversion?

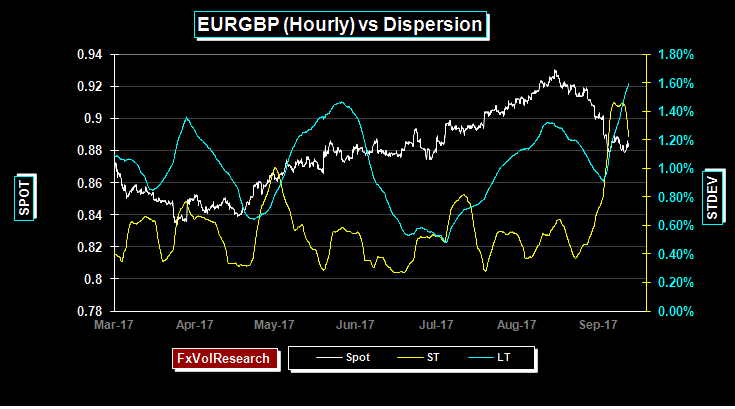

EURGBP held the 88 level during the week but LT dispersion is still rising. If 88 gives way then we can easily go all the way back to 85. On the topside, we need a close back over 90 to re-assert the EUR bull trend.

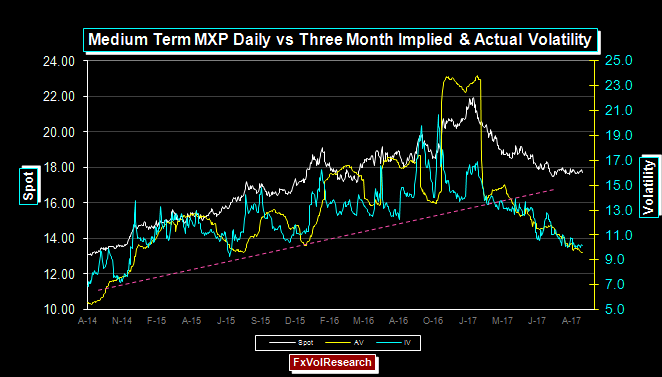

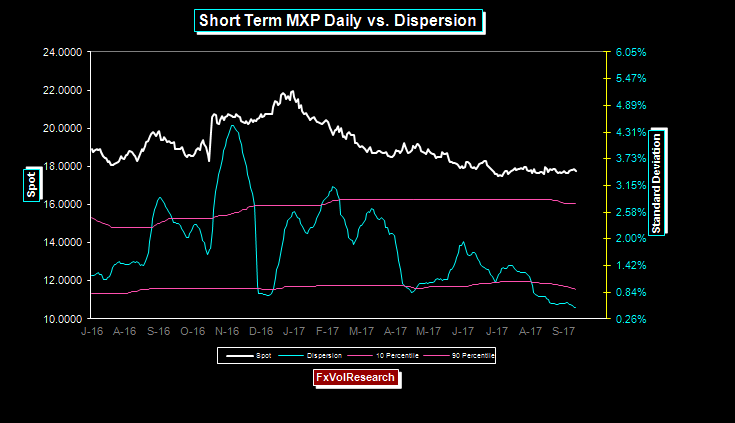

3M MXP implied vols starting to slowly rise. Notice that the spread over the actual is now positive. MXP options remain some of the least expensive in our database. 12-month MXP risk reversals remain expensive.

The MXP cannot consolidate forever. The longer the dispersion decline the more dramatic the likely trend that ensures from these level. Option strategies should be favored over forward hedges, but should also incorporate the excess skew in the back end of the curve. In our view, one year MXP puts are overpriced in relation to MXP calls.

Source: James Rider – http://bit.ly/2yoaw9P